Introduction

Tax amnesty programs are initiatives by governments to encourage taxpayers to declare previously undisclosed assets and income by offering incentives such as reduced penalties and immunity from prosecution. Indonesia has implemented two significant tax amnesty programs, known as Tax Amnesty Phase I and Phase II. This article will compare the results of these two phases, highlighting their impact on the economy and taxpayer compliance.

Overview of Tax Amnesty Programs

Tax Amnesty Phase I was launched in 2016 and aimed to increase tax compliance and boost government revenue by allowing taxpayers to declare previously unreported assets. The program offered reduced penalties and immunity from prosecution for those who participated.

Tax Amnesty Phase II, also known as the Voluntary Disclosure Program (PPS), was implemented in 2022. This phase targeted taxpayers who had not fully disclosed their assets during the first phase or had acquired new assets that were not reported. The program aimed to further enhance tax compliance and increase government revenue.

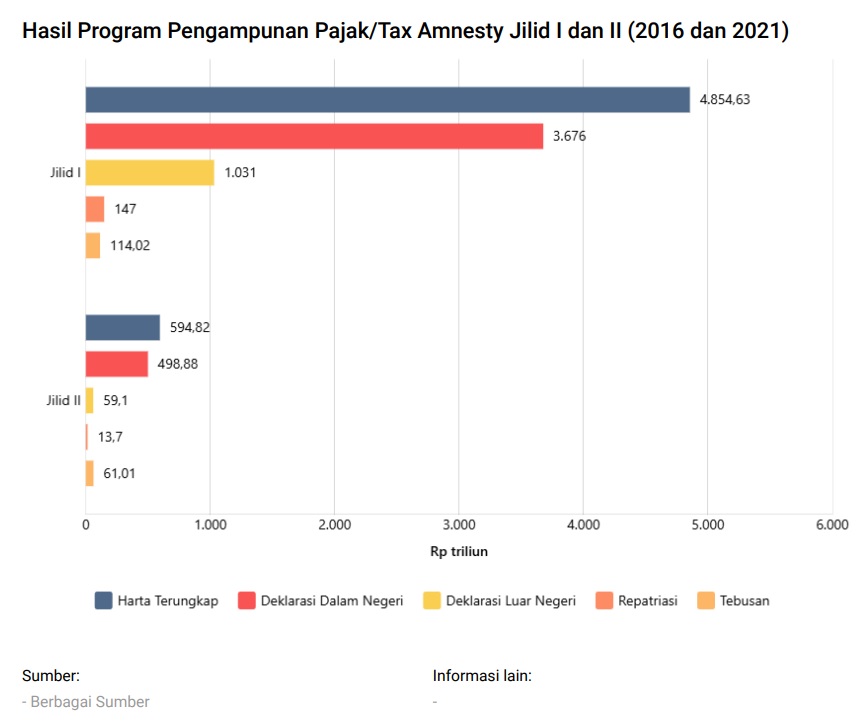

Results of Tax Amnesty Phase I

Tax Amnesty Phase I was considered a success, with significant participation from taxpayers. Key results include:

- Total Assets Declared: Taxpayers declared a total of IDR 4,866 trillion in assets. This included both domestic and overseas assets.

- Government Revenue: The program generated IDR 114 trillion in additional tax revenue.

- Number of Participants: Approximately 956,000 taxpayers participated in the program.

- Impact on Compliance: The program improved tax compliance by encouraging taxpayers to regularize their tax affairs and report previously undisclosed assets.

Results of Tax Amnesty Phase II

Tax Amnesty Phase II, or PPS, also achieved notable results, although on a smaller scale compared to the first phase. Key outcomes include:

- Total Assets Declared: Taxpayers declared a total of IDR 594.82 trillion in assets. This included domestic declarations, repatriated assets, and overseas declarations.

- Government Revenue: The program generated IDR 61.1 trillion in additional tax revenue.

- Number of Participants: Approximately 247,918 taxpayers participated in the program.

- Impact on Compliance: The program continued to enhance tax compliance by targeting taxpayers who had not fully disclosed their assets during the first phase or had acquired new assets.

Comparison of Phase I and Phase II

When comparing the results of Tax Amnesty Phase I and Phase II, several key differences and similarities emerge:

- Scale of Participation: Phase I saw a higher number of participants (956,000) compared to Phase II (247,918). This difference can be attributed to the broader scope and initial novelty of the first phase.

- Total Assets Declared: The total assets declared in Phase I (IDR 4,866 trillion) were significantly higher than in Phase II (IDR 594.82 trillion). This reflects the initial impact of the first phase in uncovering a large volume of previously undisclosed assets.

- Government Revenue: Phase I generated more revenue (IDR 114 trillion) compared to Phase II (IDR 61.1 trillion). The higher revenue in Phase I is consistent with the larger volume of assets declared.

- Focus and Target: Phase II specifically targeted taxpayers who had not fully disclosed their assets during Phase I or had acquired new assets. This narrower focus resulted in fewer participants but still contributed to improving overall tax compliance.

Factors Contributing to the Success of Tax Amnesty Programs

Several factors contributed to the success of Indonesia’s tax amnesty programs:

- Incentives for Participation: Both phases offered reduced penalties and immunity from prosecution, which encouraged taxpayers to come forward and declare their assets.

- Government Support: Strong support from the government and clear communication about the benefits of participation helped build trust and encourage compliance.

- Public Awareness Campaigns: Extensive public awareness campaigns educated taxpayers about the programs and their benefits, leading to higher participation rates.

- Technological Advancements: The use of technology in processing declarations and managing data improved the efficiency and effectiveness of the programs.

Challenges and Lessons Learned

Despite their success, the tax amnesty programs also faced challenges:

- Skepticism and Trust Issues: Some taxpayers were skeptical about the government’s ability to maintain confidentiality and feared potential repercussions.

- Complexity of Regulations: The complexity of tax regulations and the process of declaring assets deterred some taxpayers from participating.

- Sustainability of Compliance: Ensuring long-term compliance beyond the amnesty periods remains a challenge. Continuous efforts are needed to maintain and improve tax compliance.

Conclusion

Indonesia’s Tax Amnesty Phase I and Phase II have significantly contributed to increasing tax compliance and government revenue. While Phase I had a broader impact with higher participation and revenue, Phase II continued to build on this success by targeting specific taxpayers and further enhancing compliance. The lessons learned from these programs highlight the importance of incentives, government support, public awareness, and technological advancements in achieving successful tax amnesty initiatives. Moving forward, continuous efforts are needed to sustain and improve tax compliance, ensuring a robust and transparent tax system.